December 5th, 2011

Courtesy of The Oil Drum, an in-depth look at Azerbaijan:

“…Azerbaijan sits in a region of states along the southern Russian border that show the promise of holding some of the last large deposits of fossil fuel yet to be fully developed.

Location of Baku, and Azerbaijan (Google Earth) The first fields to be developed were the onshore Balakhany, Sabunchi and Ramany in 1871, with the coastal field of Bibi-Eybat being developed in 1873. Such was the nature of prospecting at the time, and the multiplicity of oil-bearing layers in the ground, this oil still remains to be found and recovered. It has been estimated that the fields initially held around 8 billion barrels of oil (John Grace), but while a billion of this was within range of early technology, the rest waited for the more advanced western technologies to arrive, though sometimes these didn’t.

As a result, new wells have been sunk in these old fields within the last year. One at Balakhany is aimed to be 3,200 ft deep, with a target production of 28 barrels a day. Most of the production followed the Russian Civil War and in the lead into World War II. In 1913 production was at 206 kbd but fell to 81 kbd by 1921, and then slowly built until the region was producing 622 kbd by the start of the war.

Balakhany today (Alexander Zaitchik) The older fields no longer have the reserves to justify the investment of the large capital equipment associated with modern technology, but their history describes the wealth that they produced before the World War I, first for the Nobel family and then for the Rothschilds. Baku oil also underwrote the career of Mr “Five Percent” Calouste Gulbenkian. Daniel Yergin notes that it was the need to replace expensive British coal that led Russia to use oil, first in ship bunkers on the Black Sea and then to fuel the railway engines across Russia. However, production continued to fall from the original wells at Baku; Royal Dutch/Shell had bought out the Rothschilds, yet in the period just before WWI, Russia’s export market share had dropped below 10% as the shallow fields ran out. Of course this was also the time that Stalin was learning his trade as an organizer/agitator in the Baku fields, though it was not until 1920 that the Bolsheviks took Baku and nationalized the oil industry.Azerbaijan remains, however, along with the fields off the peninsula, the source of a growing percentage of global production. Because of that, this is where the Baku-Tiblisi-Ceyhan pipeline begins. The BTC pipeline carries up to 1.2 mbd of oil to the Turkish port of Ceyhan on the Mediterranean where it can be loaded into tankers.

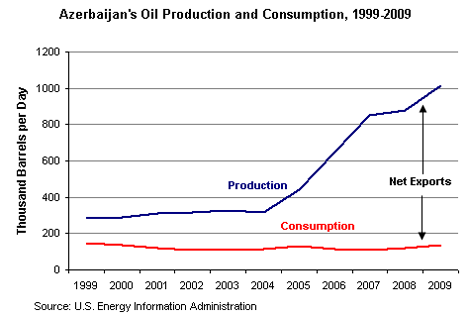

Path of the BTC pipeline (Central Asia-Caucasus Institute) To meet this and other demands, the re-growth of the oil industry in Azerbaijan has, within the last decade, raised production from 283 kbd to more than 1 million bd.The most productive of these fields lies 62 miles east of Baku in the Caspian, where the complex of fields known as the Azeri-Chirag-Gunashli (ACG) field lies. The complex is believed to hold 9 billion barrels of oil, though these are only a few of the fields found in the region. Yet there is a world of difference between how these fields are being developed with modern equipment and investment and the fate of the older fields. The oilfields of Azerbaijan (Offshore Technology) It is here also that the Shah Deniz field, with 22 Tcm of natural gas and 750 mb of oil can be found.The region has thus not only had but continues to have significant fossil fuel reserves. Production this year averaged 989 kbd to date, with $19 billion in exports of 715 kbd. This is up from last year, but down from the 2009 figures.

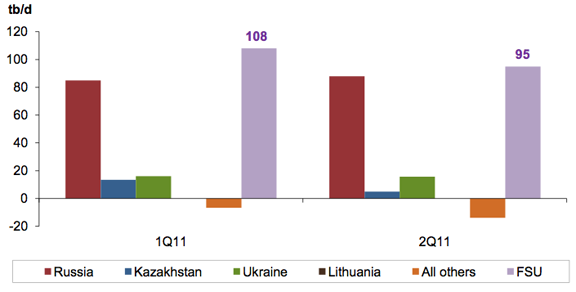

As the volume of oil available has increased, so the market for Azeri oil has also grown. Azerbaijan began exporting oil to India this year, and already sends some to China. It plans on sending oil to Czech and Ukrainian refineries and to Slovakia to the tune of around 15 million barrels a year. The diversion of more oil to countries of the Former Soviet Union is something that has caught OPEC attention, and they note in their November MOMR that the booming Russian economy is increasing internal demand, with a consequent cost to exports to the tune of around 100 kbd growth in demand in the FSU to 4.2 mbd.

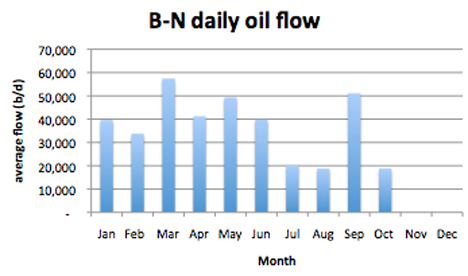

FSU oil demand change (y-o-y) in kbd for selected countries (OPEC November MOMR) In terms of natural gas production, the IEA projects that this will grow from a current 17 billion cubic meters (bcm) a year to 50 bcm by 2035, much of this to come from the second phase of the development of Shah Deniz.In this regard it should be remembered that there are three main oil pipelines that carry oil out of Azerbaijan and while the BTC carries the majority, the Baku-Novorossiysk pipeline (B-N) carries 7% of the exports to the Black Sea Russian port of Novorossiysk, and the Baku-Supsa pipeline carries 14% of the total feeding oil to the Georgian port of Supsa, with a capacity of 145 kbd. The flows from Azerbaijan to Russia, via the B-N pipeline have been fluctuating all year, but on average have fallen over 12% from last year.

Average monthly flow in the pipe from Azerbaijan to Russia (News.AZ) It may be that, in the same way Russia used to play with demand for gas from Turkmenistan, they are now playing the same game of cutting back demand in order to force lower prices. However, as with the Chinese pipeline to Turkmenistan, the BTC pipeline from Baku provides other customers so that prices may now be maintained – and with these, support for the local governments. (The Azerbaijan government now has a strategic reserve of $41 billion).

Focusing primarily on The New Seven Sisters - the largely state owned petroleum companies from the emerging world that have become key players in the oil & gas industry as identified by Carola Hoyos, Chief Energy Correspondent for The Financial Times - but spanning other nascent opportunities around the globe that may hold potential in the years ahead, Wildcats & Black Sheep is a place for the adventurous to contemplate & evaluate the emerging markets of tomorrow.