An industrial zone should be a noisy place. At the Zona Económica Especial (zee), a Manhattan-sized plot near Luanda, Angola’s capital, the only sound is birdsong. “My boss said to only show you the factories that are working,” a guide tells your correspondent. Yet all is not well at a handpicked pipe manufacturer. It operates at 10% capacity. Power has just gone out, so unfinished tubes droop out of machines, like saggy wizard sleeves. “Would you like to take a photo of a worker pretending to use the machine?” asks the guide.

ZEE is a monument to Angola’s gigantism, corruption and folly. The country is sub-Saharan Africa’s third-largest economy and its second-largest oil exporter. From 2002, when 27 years of on-off civil war ended, until 2015, gdp grew by almost 10% a year, a result of high oil prices and a surge in production. But little wealth trickled down to ordinary Angolans, nearly two-thirds of whom live on less than $2 a day. The elite in the ruling mpla party stole or squandered billions on projects such as the zee. In the zone the state runs 73 factories, which splurge on everything from machines to uniforms without a nod to cost.

After becoming president in September 2017 João Lourenço vowed to stop such idiocy, overhaul the economy and tackle corruption. He surprised many observers by swiftly sacking the super-rich children of his predecessor, José Eduardo dos Santos, from the top jobs at Sonangol, the state oil company, and Angola’s sovereign-wealth fund. The ex-president’s son, José Filomeno dos Santos, was charged with fraud and money-laundering, which he denies.

The purge raised expectations. On WhatsApp Angolans shared images of “The Terminator”, with Mr Lourenço as Arnold Schwarzenegger. But the new president prefers another analogy. Last year he likened himself to Deng Xiaoping, the politician who led China’s economic reforms in the 1980s. This is revealing, says Ricardo de Soares Oliveira of Oxford University. For Mr Lourenço, Deng was someone who saw reform as a means to an end: a way of keeping the ruling party in power.

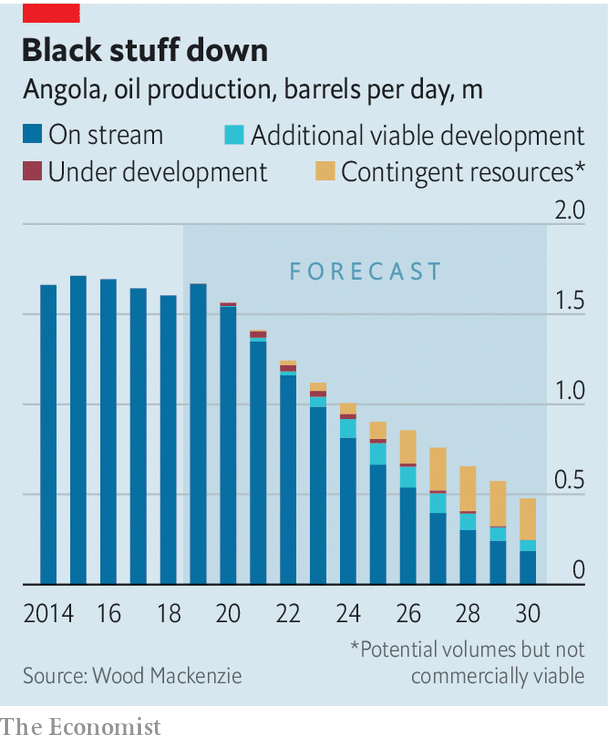

Angola has little option but to reform. Oil accounts for about 95% of exports and half of government revenues. But relatively low oil prices mean that the economy has lagged behind population growth since 2015, and will continue to do so until at least 2019. Even if oil prices recover, Angola is set to sell less of the black stuff. Production is forecast to fall from 1.6m barrels per day in 2018 to 0.7m in 2028 (see chart). “We can no longer depend on oil,” says José Massano, the governor of the central bank.

Under Mr dos Santos “diversifying” the economy meant Potemkin projects like the zee. Mr Lourenço, instead, plans to privatise 50-100 companies, including many in the Sonangol empire. A new law removes the need for foreign investors to have an Angolan partner, a rule that had created a cadre of useless but well-connected “tenderpreneurs” during the boom years.

In January Angola stopped pegging its currency (the kwanza) to the dollar, relieving pressure on foreign reserves. The central bank now auctions dollars instead of handing them to cronies.

The authorities are also trying to clean up Angola’s financial system. Most banks in Angola are, in fact, not banks in the normal sense, says Carlos Rosado de Carvalho, the editor of a business newspaper. As recently as 2009, 85% of all lending went to about 200 individuals. Business plans can amount to “I need $5m now,” sighs one bank executive. Nearly 29% of loans are in default. The central bank has raised capital requirements, introduced new accounting standards and suspended the board of one of the worst-run state banks.

Whereas Mr dos Santos made Angola the main recipient of Chinese lending in Africa, Mr Lourenço has sought to rebalance its foreign relations. He has visited Belgium, France, Germany and Portugal. Perhaps the clearest sign of change is Angola’s improved relationship with the imf. Under Mr Lourenço Angola has adopted many of the fund’s recommendations and is set to borrow money from it in the next few months.

His reforms are encouraging. But it is too soon to get carried away. He has barely begun to mend the harm caused by his awful predecessor. More years of slow growth and inflation in the double digits will test the patience of Angolans ahead of local elections in 2020.

It is also too early to judge his anti-corruption efforts. Mr Lourenço remains a party man. And many mpla bigwigs would hate to see corruption curbed. Since taking power after independence from Portugal in 1975, the mpla has proved remarkably adaptive. During the cold war it embraced communism; as its Soviet sponsor crumbled it turned to crony capitalism and multiparty elections. At no point have its leaders shown much interest in the welfare of ordinary Angolans. It is possible, alas, that Mr Lourenço’s appointees may see the new order as their chance to get rich quick.

Nor has Mr Lourenço shown himself to be much of a political reformer. He has rejected calls to change the constitution to limit his powers. He has put loyalists in key positions in the army and security services. And he has shown little desire to make courts independent. Such omissions undermine his talk of a new Angola. “We don’t need a strongman,” says a local activist. “We need strong institutions.”

This entry was posted on Monday, December 10th, 2018 at 3:34 am and is filed under Angola. You can follow any responses to this entry through the RSS 2.0 feed.

Both comments and pings are currently closed.

Comments are closed.

ABOUT

Wildcats & Black Sheep is a personal interest blog dedicated to the identification and evaluation of maverick investment opportunities arising in frontier - and, what some may consider to be, “rogue” or “black sheep” - markets around the world.

Focusing primarily on The New Seven Sisters - the largely state owned petroleum companies from the emerging world that have become key players in the oil & gas industry as identified by Carola Hoyos, Chief Energy Correspondent for The Financial Times - but spanning other nascent opportunities around the globe that may hold potential in the years ahead, Wildcats & Black Sheep is a place for the adventurous to contemplate & evaluate the emerging markets of tomorrow.