February 9th, 2023

Via Geopolitical Futures, a look at how Mexico will benefit from Washington’s focus on building a North American semiconductor supply chain:

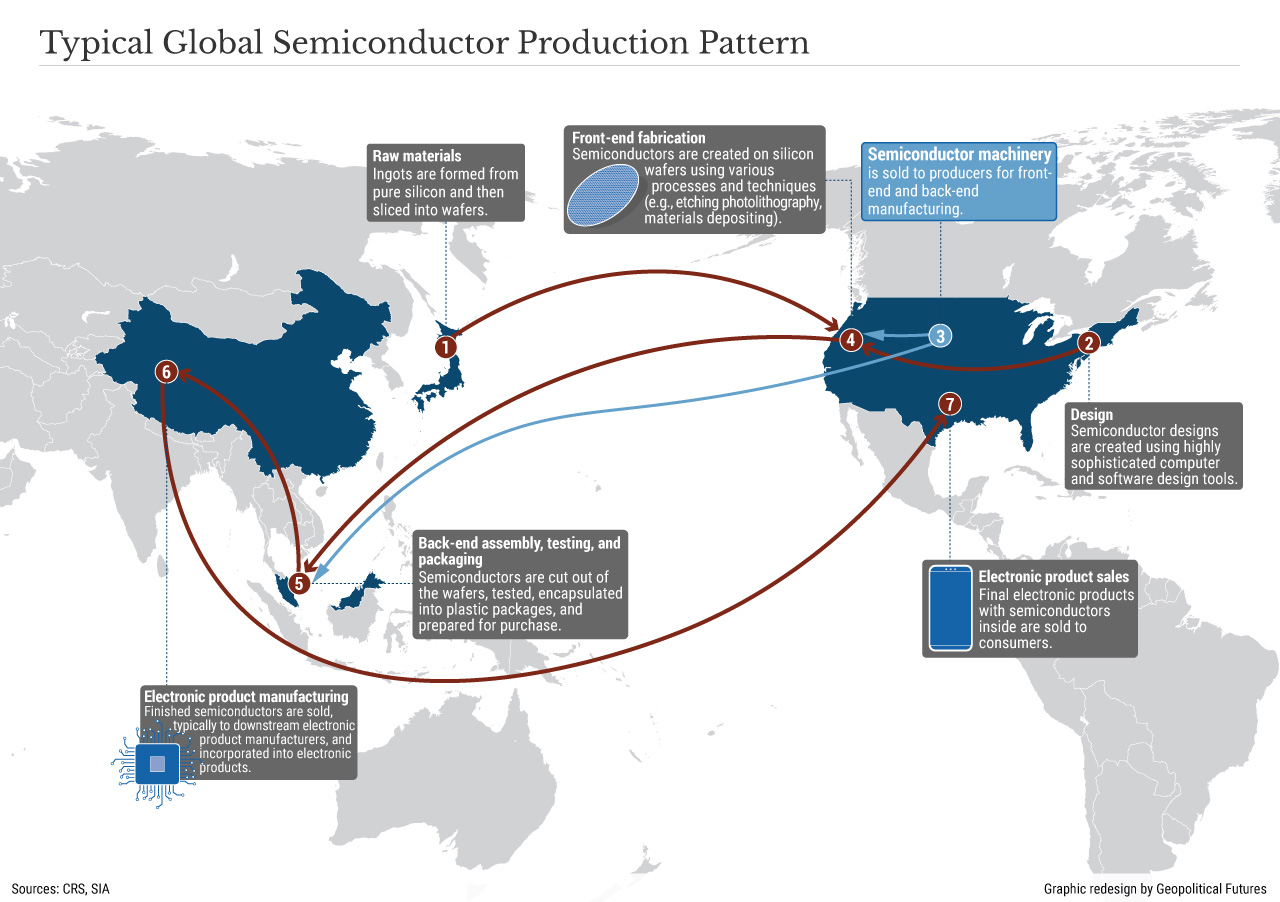

The United States is prioritizing the creation of a regional semiconductor production chain to give itself alternatives to Asian firms, especially those with ties to China. Even for the country that invented the semiconductor, this is a massive task. The manufacture of cutting-edge chips is incredibly expensive and complicated, and just a few companies around the world are dominant. If the U.S. is going to succeed in its chips drive, it will need to involve Mexico.

Chip Race

Today, semiconductors are used in everything from consumer goods (computers, cellphones, automobiles, etc.) to military equipment and communication satellites. But despite the ubiquity of chips in modern technology, the manufacturing equipment for more than three-quarters of the global chip supply comes from just five companies. Three of these firms (Applied Materials, Lam Research Corp. and KLA Corp.) are in the United States, and the other two are in U.S. allies: the Netherlands’ ASML and Japan’s Tokyo Electron. ASML holds a monopoly on the machinery needed to make the most advanced semiconductors.

The U.S. is determined to defend and extend this advantage over China. In 2022, Washington passed the CHIPS and Science Act, which allotted $52.7 billion for the research, development and manufacturing of microchips. It also passed the Inflation Reduction Act, which supports the manufacture of electric vehicles and relevant chips in North America. Internationally, the U.S. in late January convinced Japan and the Netherlands to work with it on restricting semiconductor technology sales to China. This builds on a 2019 agreement that banned ASML from exporting its most advanced machinery to China. The latest agreement expands these restrictions, although details have not been released. The U.S. is likely trying to strike a balance between pressuring China and not spurring Beijing to accelerate development of domestic capabilities.

Over time, Washington wants to reduce its own reliance on foreign firms, particularly those tied to China as well as companies like ASML. According to the Semiconductor Industry Association, from 1990 to 2021, the U.S. share of global semiconductor manufacturing capacity fell to 12 percent from 37 percent. Most of it is now in Asia. The U.S. is now trying to coax chipmakers into moving to North America. Major players like GlobalFoundries, Intel, Samsung Foundry, TSMC and Texas Instruments are building new semiconductor production facilities in the United States, especially New York, Texas, Arizona and New Mexico. Washington is mainly focused on the automotive sector, where the U.S. is highly integrated with Canada and Mexico. This sector plays a major role in driving the U.S. and Mexican economies. The three countries agreed to develop a joint chipmaking initiative, including coordinating supply chains and investments. They also want to work together to map critical minerals.

Mexico’s Advantages

About 40 percent of U.S. semiconductor plants are in states along its southern border, a significant opportunity for Mexico. Likewise, many of Mexico’s manufacturing hubs, especially for high-end manufacturing and automobiles, are in northern border states. Mexico’s foreign minister estimates that a quarter or more of imports from Asia could be replaced by North American production, boosted by the U.S.-Mexico-Canada free trade agreement.

The Mexican government has already begun laying the diplomatic groundwork to support its chip ambitions. At the beginning of the year – prior to the U.S.-Japan-Netherlands agreement – Japan’s foreign minister was in Mexico discussing trade and semiconductors. Later in January, a Dutch delegation along with U.S. officials visited the northwestern Mexican state of Baja California for talks on investment opportunities, with a focus on agro-industry, electric vehicles, semiconductors, supply chains and energy.

Talks are also underway between the Mexican government and the business community. Firms like Intel, Skyworks Solutions, Texas Instruments and Infineon Technologies are already operating in Mexico and working on chip R&D and test manufacturing. Conversations with Taiwanese chipmakers like TSMC are ongoing. Foxconn, the world’s biggest contract electronics manufacturer, already established a headquarters in Mexico in order to be closer to clients (mostly in the electronic vehicles sector) in North America. Mexico is also working with the Inter-American Development Bank to identify semiconductor opportunities, and with the National College of Professional Technical Education to produce more skilled workers to serve in chip manufacturing. Finally, Mexican industry and higher education institutions have partnered with Arizona State University to boost the production of semiconductors in North America through training and increased production capacity in northwest border states.

Some in Mexico hope that Washington’s semiconductor drive will help develop the country’s southern region. This would help the government solve one of its biggest challenges, but the initiative is no quick fix. Currently, Mexico’s chip industry is limited to lower-skill roles like assembly, testing and packaging – ideal starting points for the development of more skilled, formal work in Mexico’s underdeveloped south. Moreover, chipmaking uses large amounts of water, which is more plentiful in southern Mexico. But although the south is close to the narrow Isthmus of Tehuantepec, giving exporters quick access to the Atlantic and Pacific, its transportation (and energy) infrastructure is poor. Existing Mexican industrial complexes, particularly for automobiles, are farther north, in Guadalajara, Nuevo Leon, Baja California, Aguascalientes and Chihuahua. Semiconductor manufacturing will probably stay close to these clusters to leverage existing infrastructure and shorter distances to the United States.

Rules and Rivals

While Mexico is on paper a promising location for chipmakers, there are several challenges it must address to play a major role in the U.S. semiconductor manufacturing chain. First, the U.S. and Mexico are at odds over the government’s management of the electricity sector. A stable and secure electricity supply is critical for chipmaking, but future investments in the Mexican electricity network are in jeopardy because of these disputes, which adds risk for manufacturers. Similarly, U.S. companies have taken issue with Mexico’s labor laws. This recurring point of contention generally occurs at the company or plant level and cannot be ruled out. Foreign firms also want Mexico to alter its regulations and incentives to make itself a better business environment for semiconductor manufacturing.

However, the main threat to U.S.-Mexican cooperation is increasing Chinese investment in Mexico. The U.S. will expect Mexico to restrict Chinese firms from entering the Mexican segments of the North American chip supply chain. This is a major reason Washington wants much closer coordination with Mexico City on strategic goods. It is also why the U.S. is starting with less sophisticated chips used in things like cars rather than high-end products related to defense. The U.S. can leverage its relationships with Japan and South Korea – which already relocated some manufacturing to Mexico – to encourage non-Chinese investment in the country. And of course, the U.S. can threaten to restrict investment, trade, remittances, etc. to its southern neighbor to drive its point home.

None of Mexico’s challenges are insurmountable. And the U.S. interest in becoming self-sufficient in semiconductor production, as well as the importance of the auto industry to the U.S. economy, means the U.S. will be very willing to work with Mexico to find solutions.

Focusing primarily on The New Seven Sisters - the largely state owned petroleum companies from the emerging world that have become key players in the oil & gas industry as identified by Carola Hoyos, Chief Energy Correspondent for The Financial Times - but spanning other nascent opportunities around the globe that may hold potential in the years ahead, Wildcats & Black Sheep is a place for the adventurous to contemplate & evaluate the emerging markets of tomorrow.