The Soda War: How a Coca Cola, Pepsi, and M&M Ingredient is Fueling Conflict in Sudan April 10th, 2026

Via The Africa Report, commentary on how gum arabic – the ingredient that puts the gloss in Coke, Pepsi and M&Ms – is fuelling the conflict in Sudan

In Sudan, in the savannahs of Kordofan and Darfur, millions of families depend on the acacia tree for their livelihood. They score its bark and collect the sap, which hardens into amber-coloured tears.

Once dried and processed into a fine white powder, it ends up in a can of Coca-Cola, a packet of M&Ms or cigarette paper. Acacia is everywhere, under the name “E414” – a code that sounds industrial, yet gum arabic is entirely natural.

It comes from the sap of a shrub that grows across the Sahel belt, where almost nothing else survives.

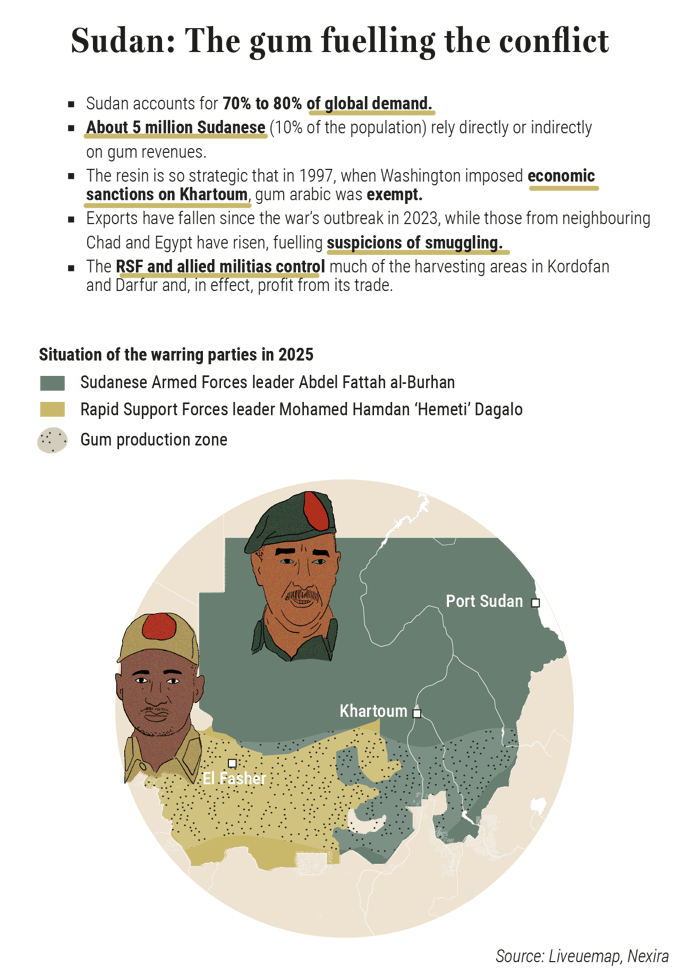

An emulsifier, stabiliser, binding agent – entire sectors of industry depend on it. The food industry alone accounts for more than half of global production (around 100,000 tonnes per year), driven by beverages and confectionery.

No chemist has yet succeeded in synthesising it. The resin is so strategic that Washington granted it an exemption from the sanctions imposed on Khartoum as early as 1997 – a highly unusual concession, secured under pressure from major American soft drinks companies.

This resin, with its countless properties, is also one of the fuels of the civil war that has been tearing Sudan apart since April 2023, when the Rapid Support Forces (RSF) led by General Mohamed Hamdan Dagalo – known as Hemeti – attacked the regular army loyal to Abdel Fattah al-Burhan in Khartoum. In three years, the conflict has claimed more than 150,000 lives.

A substitute for soldiers’ wages

The RSF and their allied militias now control most of the production areas – namely Kordofan and Darfur, where they stand accused of genocide – which account for three-quarters of Sudan’s harvest. The warring parties are seeking to extract maximum profit from the chaos: each side attempts to sell output from the territories it controls, armed groups levy taxes on transporters, and smuggling networks are being reorganised.

Between January and June 2024, traders in Darfur confirmed the theft of 3,700 tonnes of gum, worth around $14.6m, looted by the RSF and their allied militias, according to the UN. Commanders acknowledged these raids, tolerating them as a substitute for wages, with some soldiers having gone unpaid for nearly a year. The stolen gum was then routed through Chad, the Central African Republic and South Sudan.

Officially, Sudanese exports fell by nearly half in 2025, dropping to 60,000 tonnes. In reality, gum continues to be transported via neighbouring countries – Egypt in particular, a non-producing country that nevertheless appears in export statistics.

The UN Panel of Experts estimates that 50,000-70,000 tonnes pass each year through areas along the Chadian border under RSF control, and a further 30,000-40,000 tonnes head towards Libya via routes held by the regular army. Prices, meanwhile, have risen by 50%-100%, depending on quality, over three years.

Chad, Kenya, Senegal and Mali move into production

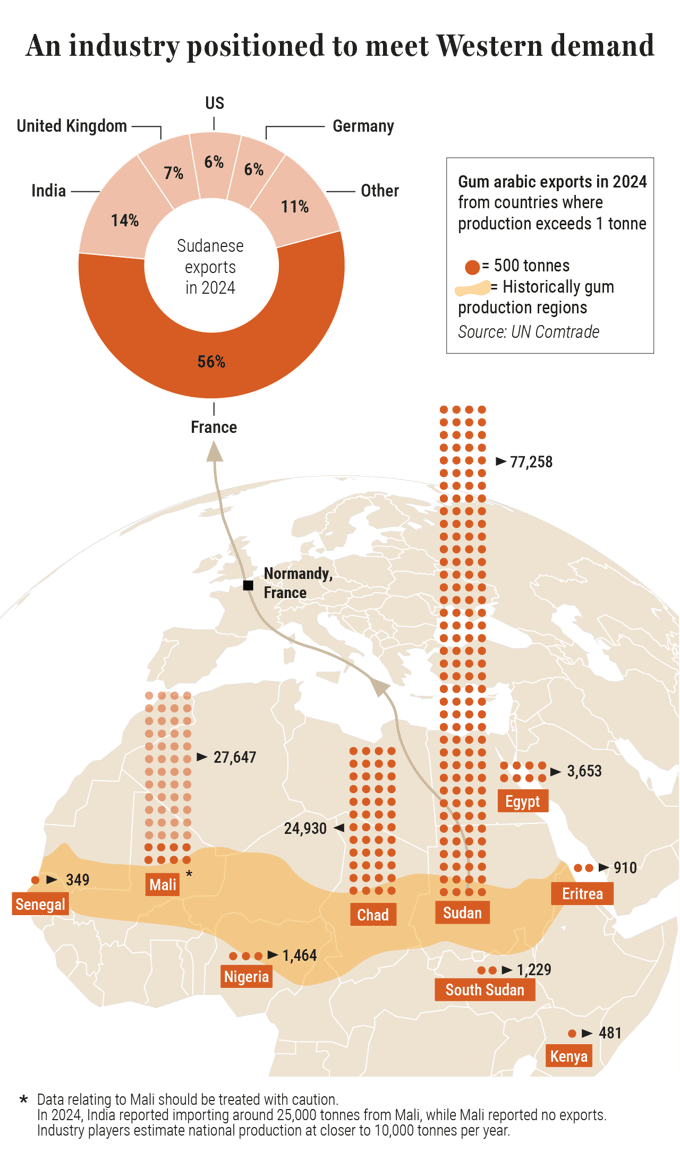

France’s two main importers, Nexira and Alland & Robert – both Normandy-based companies that together control a dominant share of the global market – acknowledge having faced difficult periods. Nevertheless, they continue to work with their long-standing suppliers, routing most of their purchases through Port Sudan, while also seeking to diversify their sources towards emerging producer countries such as Kenya.

The generals’ war has reignited interest in production from Chad, Kenya, Senegal and Mali, which are positioning themselves to meet Western demand, particularly from France. Chad saw its exports rise by more than 40% in 2024, to around 30,000 tonnes, notably thanks to competitive prices, new warehouses and improved road infrastructure.

Will industrial players in these new producing countries be able to seize this opportunity to revive the sector by investing in processing plants located in the Sahel itself, where the acacia trees have their roots?

This entry was posted on Friday, April 10th, 2026 at 6:11 am and is filed under Sudan. You can follow any responses to this entry through the RSS 2.0 feed.

Both comments and pings are currently closed.

Comments are closed.

ABOUT

Wildcats & Black Sheep is a personal interest blog dedicated to the identification and evaluation of maverick investment opportunities arising in frontier - and, what some may consider to be, “rogue” or “black sheep” - markets around the world.

Focusing primarily on The New Seven Sisters - the largely state owned petroleum companies from the emerging world that have become key players in the oil & gas industry as identified by Carola Hoyos, Chief Energy Correspondent for The Financial Times - but spanning other nascent opportunities around the globe that may hold potential in the years ahead, Wildcats & Black Sheep is a place for the adventurous to contemplate & evaluate the emerging markets of tomorrow.